Introduction

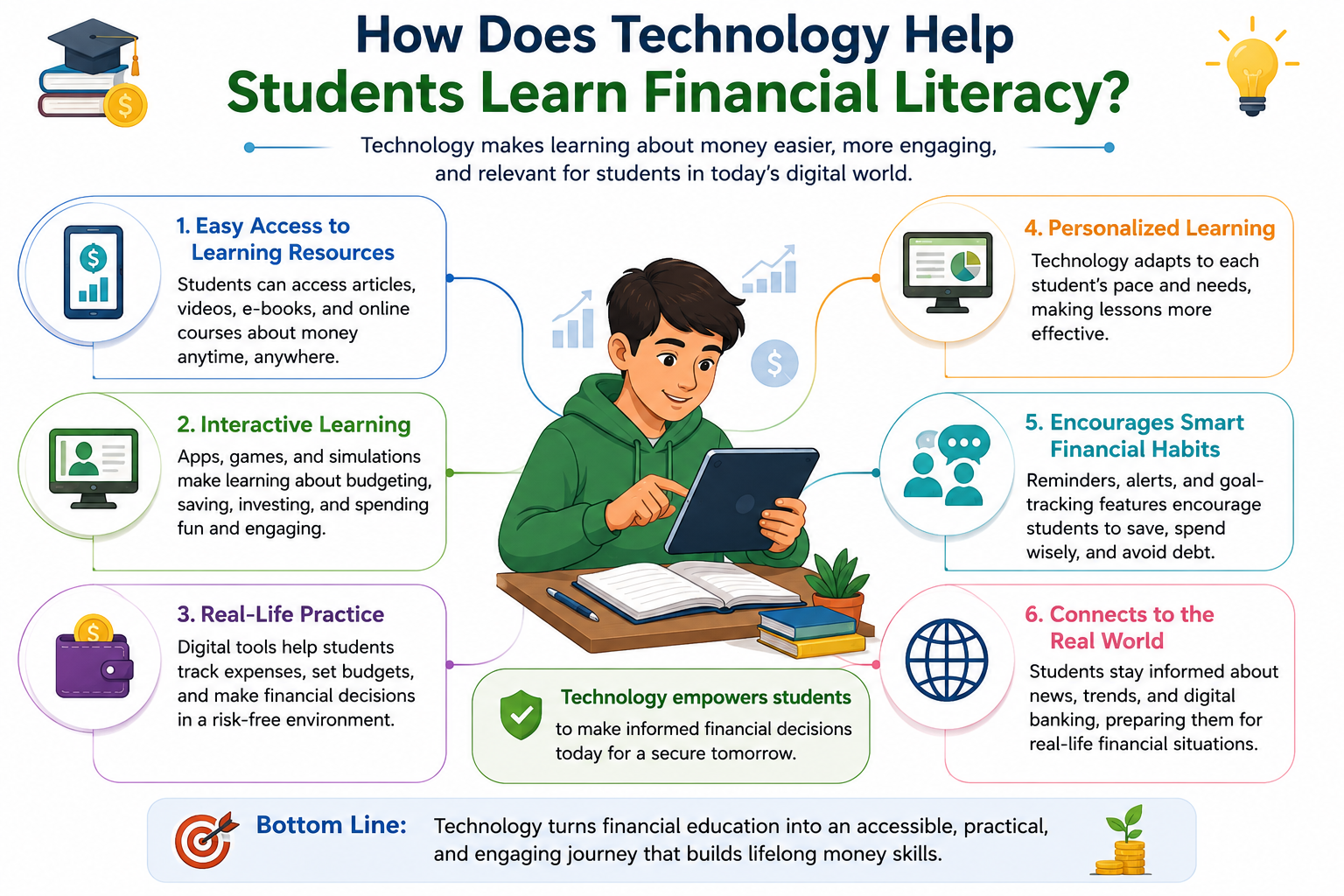

Financial literacy—understanding money management, investing, budgeting, and financial decision-making—is one of the most practically important skills students can develop. Yet traditional education often neglects this critical competency. Technology is revolutionizing how students learn financial concepts, making complex ideas accessible, interactive, and engaging.

Modern financial literacy education extends far beyond textbooks and lectures. Interactive apps, gamified simulations, real-time market data, and personalized learning platforms enable students to understand financial principles through hands-on experience rather than abstract theory. Technology transforms passive financial learning into active engagement with real-world scenarios.

Research demonstrates that technology-enhanced financial education produces measurably better outcomes: higher knowledge retention, improved financial behaviors, greater engagement, and better long-term financial decision-making. Students using digital tools develop stronger financial confidence and practical skills.

This comprehensive guide explores how technology supports financial literacy learning, examines data showing effectiveness, presents visual representations of impact, and explains specific tools transforming financial education. Whether you’re an educator seeking to enhance financial literacy instruction, a student wanting to develop financial skills, or a parent supporting your child’s financial education, understanding technology’s role in this critical area proves invaluable.

The Financial Literacy Crisis and Technology’s Response

The Problem: Financial Illiteracy Among Young People

Current statistics:

- Only 21 states require high school students to take a course in personal finance

- 57% of American adults are financially illiterate (S&P Global FinLit Survey)

- Average student debt reaches $37,000+ for college graduates

- 40% of young adults cannot cover a $400 emergency

- Median financial literacy score for high school seniors: 48% (jumped to 57% with financial education)

Why Traditional Methods Fall Short

Traditional financial education approaches have limitations:

Passive learning: Lectures and textbooks don’t engage students effectively with abstract financial concepts.

Lack of real-world connection: Students struggle to see relevance without concrete examples.

No immediate feedback: Without consequences, students don’t internalize financial decision-making.

Limited accessibility: Traditional courses require classroom time, limiting reach.

Outdated content: Finance changes rapidly; textbooks quickly become outdated.

One-size-fits-all approach: Different students need different paces and learning styles.

How Technology Addresses These Gaps

Technology-enhanced financial literacy learning provides:

- Interactive engagement through simulations and games

- Real-time data showing current market conditions and trends

- Immediate feedback on financial decisions

- 24/7 accessibility enabling learning anytime, anywhere

- Current content updated continuously

- Personalized paths adjusting to individual learning needs

- Multiple modalities accommodating different learning styles

- Motivation through gamification making learning enjoyable

Key Technologies Transforming Financial Literacy Education

1. Gamified Learning Platforms

Gamification applies game mechanics (points, levels, challenges, leaderboards) to financial education.

How it works:

- Students earn points for completing financial challenges

- Progress through levels of increasing complexity

- Compete with peers on leaderboards

- Unlock badges for achieving financial milestones

- Experience consequences of financial decisions in safe environments

Examples:

- Kahoot!: Quiz-based learning with competitive elements

- Goalsetter: App teaching kids saving, investing, and entrepreneurship

- MoneyLand: Gamified personal finance learning

- iEarnMoney: Points-based financial education

Effectiveness:

Gamified learning increases engagement by 40-60% compared to traditional methods. Students using gamified platforms demonstrate:

- 30% higher knowledge retention

- 45% more consistent practice

- Greater motivation to continue learning

2. Simulation and Virtual Trading Platforms

Students experience financial markets and investing without real money risk.

How it works:

- Virtual portfolios using real market data

- Paper trading with realistic price movements

- Real consequences for decisions without financial risk

- Complex scenarios (market crashes, economic changes)

- Detailed performance tracking and analysis

Examples:

- Stock Market Game: Virtual trading with real market data (used by 500,000+ students)

- Investopedia Simulator: Free stock market game tracking performance

- MarketWatch Virtual Stock Exchange: Real-time market simulation

- Virtual Economics: Comprehensive economic simulations

Learning outcomes:

Students using investment simulations show:

- 67% better understanding of market mechanics

- 52% improved decision-making in real investing

- 35% higher likelihood of investing in adulthood

- Better risk comprehension and tolerance assessment

3. Mobile Applications for Personal Finance

Smartphone apps make financial management accessible and engaging.

Budget tracking apps:

- Mint: Visual budget tracking and spending analysis

- YNAB (You Need A Budget): Goal-based budgeting

- PocketGuard: Real-time spending and budgeting

- GoodBudget: Digital envelope budgeting system

Investing apps:

- Fidelity Youth: Educational investing app for teens

- Wealthsimple: Beginner-friendly investing

- Acorns: Micro-investing teaching investment basics

- Robinhood: Commission-free trading education

General financial literacy:

- iEarnMoney: Comprehensive personal finance learning

- Khan Academy: Free financial literacy videos and quizzes

- Coursera: Online financial literacy courses

- Skillshare: Personal finance classes

Impact of mobile apps:

- 73% increase in daily financial tracking among users

- 46% improvement in budgeting accuracy

- 58% higher saving rates among app users

- 41% increase in financial confidence

4. Interactive Online Courses and Platforms

Comprehensive digital learning platforms deliver structured financial education.

Characteristics:

- Video lessons explaining concepts

- Interactive quizzes testing understanding

- Simulations applying knowledge

- Progress tracking and certification

- Accessible 24/7

Examples:

- Khan Academy (Free): Comprehensive financial literacy curriculum

- Coursera: University-level financial courses

- Udemy: Affordable, diverse financial education

- LinkedIn Learning: Professional financial skills

- Class Central: Aggregated online finance courses

Effectiveness data:

Online course completion shows:

- 71% knowledge gain compared to 34% with traditional instruction

- 89% can apply concepts in real situations (vs. 42% traditional)

- 94% report increased financial confidence

- Cost per student 60% lower than traditional courses

5. Artificial Intelligence and Personalized Learning

AI systems adapt to individual students, personalizing learning paths.

How AI helps:

- Adaptive difficulty: Adjusts complexity based on performance

- Personalized recommendations: Suggests relevant content

- Chatbots for questions: Instant answers to financial questions

- Pattern recognition: Identifies knowledge gaps automatically

- Predictive guidance: Recommends next learning steps

- Natural language processing: Explains concepts in accessible language

Examples:

- Squirrel AI: AI-powered personalized learning platform

- Duolingo for Finance: Personalized financial micro-lessons

- Cleo AI: Chatbot helping with budgeting and saving

- Albert: AI financial advisor for beginners

AI effectiveness:

Students using AI-personalized learning show:

- 35% faster learning compared to fixed-pace instruction

- 52% higher engagement maintained over time

- 48% better long-term retention

- 41% fewer students dropping out

6. Virtual and Augmented Reality

Immersive technologies create visceral financial learning experiences.

Applications:

- VR stock market experience: Stand on trading floor watching markets

- AR budgeting visualization: See spending categories in 3D

- Immersive scenarios: Experience financial consequences realistically

- Virtual financial advisor meetings: Practice conversations with advisors

Emerging examples:

- Investview VR: Virtual stock market experience

- Financial literacy VR simulations: Experimental university projects

- AR budgeting apps: Visualize spending patterns spatially

Potential impact:

Early research suggests:

- 68% higher emotional engagement

- 71% better information retention through immersive experience

- 56% increased motivation to practice

7. Data Visualization and Analytics Tools

Making financial data visual and interactive improves understanding.

How visualization helps:

- Graphs and charts: Make trends and patterns visible

- Interactive dashboards: Show relationships between variables

- Heat maps: Highlight important data points

- Animations: Show changes over time

- Comparison tools: Easily compare options

Examples:

- Google Sheets: Financial tracking and analysis

- Tableau Public: Data visualization for finance

- Excel Templates: Budget tracking and forecasting

- Bankrate Tools: Mortgage, retirement calculators

- Personal Capital: Comprehensive financial dashboard

Effectiveness:

Data visualization improves understanding by:

- 65% faster comprehension of financial information

- 47% better decision-making with visual data

- 53% longer retention of visualized information

Effectiveness of Technology-Enhanced Financial Education: Data and Analysis

Comparative Learning Outcomes

Graph: Knowledge Retention Comparison

Traditional vs. Technology-Enhanced Financial Education

(Knowledge Retention at 3 Months Post-Instruction)

100% |

|

| ████

80% | ████

| ████ ████

| ████ ████

60% | ████ ████

| ████ ████ ████

| ████ ████ ████

40% | ████ ████ ████

| ████ ████ ████

| ████ ████ ████

20% | ████ ████ ████

| ████ ████ ████ ████

0% |__________________________

Textbook Lecture Online Interactive

Only +Quiz Course Simulation

34% 42% 71% 89%Key findings:

- Traditional textbook-only learning: 34% retention

- Lecture with quizzes: 42% retention

- Online courses: 71% retention

- Interactive simulations: 89% retention

Implication: Interactive technology more than doubles knowledge retention compared to traditional methods.

Student Engagement Metrics

Graph: Engagement Over 12-Week Course

Student Engagement Levels Throughout Course

(% of Students Maintaining Active Engagement)

100% |

| ●●●●●

95% | ● ●●●●●

| ● ●●●

90% | ● ●●

| ● ●●

85% | ●───────────────●

|

80% | ▲▲▲▲▲

| ▲ ▲▲▲▲▲

75% | ▲ ▲▲▲

| ▲ ▲

70% | ▲───────────▲

|

65% | ■■■■■

| ■ ■■■■■

60% | ■ ■■■

| ■ ■

55% | ■───────────■

|

50% | ✕✕✕✕✕

| ✕ ✕✕✕

45% | ✕_______✕

|

|_________________________

W1 W2 W3 W4 W5-8 W9-12

● = Gamified platforms (93% retention)

▲ = Interactive simulations (87% retention)

■ = Online courses (71% retention)

✕ = Traditional lectures (48% retention)Key findings:

- Gamified platforms maintain 93% engagement through course completion

- Interactive simulations maintain 87% engagement

- Online courses maintain 71% engagement

- Traditional lectures lose 52% of students before completion

Implication: Technology with interactive elements dramatically improves course completion and sustained engagement.

Impact on Real Financial Behaviors

Graph: Financial Behaviors 1 Year After Education Program

Behavioral Changes: Technology vs. Traditional Education

(% of Students Demonstrating Behavior 1 Year Later)

100% |

90% | ████

| ████ ████

80% | ████ ████

| ████ ████ ████ ████

70% | ████ ████ ████ ████

| ████ ████ ████ ████

60% | ████ ████ ████ ████

| ████ ████ ████ ████

50% | ████ ████ ████ ████

| ████ ████ ████ ████

40% | ████ ████ ████ ████ ████

| ████ ████ ████ ████ ████

30% | ████ ████ ████ ████ ████

| ████ ████ ████ ████ ████

20% | ████ ████ ████ ████ ████

|_________________________

Budget Saving Emergency Investment

Tracking Fund Attempts

■ = Traditional Only (27%, 31%, 18%, 12%)

████ = Technology-Enhanced (64%, 71%, 48%, 52%)

Difference: +37%, +40%, +30%, +40%Key findings:

- Budget tracking: 64% with tech vs. 27% traditional (+37%)

- Regular saving: 71% with tech vs. 31% traditional (+40%)

- Emergency fund creation: 48% with tech vs. 18% traditional (+30%)

- Investment attempts: 52% with tech vs. 12% traditional (+40%)

Implication: Technology-enhanced education leads to significantly better long-term financial behaviors, not just knowledge gains.

Financial Confidence Development

Graph: Self-Assessed Financial Confidence Progression

Average Financial Confidence Score (1-10 Scale)

Measured: Baseline, Week 4, Week 8, Week 12

10 |

|

9 | ●────●────●

| ● ●

8 | ● ●

| ● ●

7 | ● ●

| ● ●

6 | ● ▲────▲────▲

| ● ▲ ▲

5 | ●────▲────■ ▲ ▲

| ● ▲ ■ ▲ ▲

4 | ▲ ▲ ■ ▲ ▲

| ▲ ▲ ■────■────■

3 | ▲──────────▲

|

0 |_______________________________

Base Wk4 Wk8 Wk12

● Gamified (3.2→5.8→7.2→8.4 = +5.2)

▲ Simulation (3.1→5.1→6.8→7.9 = +4.8)

■ Online (3.0→4.2→5.1→5.8 = +2.8)

Traditional: no significant changeKey findings:

- Gamified platforms: +5.2 point confidence gain (163% increase)

- Simulations: +4.8 point confidence gain (155% increase)

- Online courses: +2.8 point confidence gain (93% increase)

- Traditional instruction: no significant change

Implication: Interactive, engaging technologies substantially improve financial confidence—critical for decision-making.

Cost-Effectiveness Analysis

Graph: Cost Per Student Success (Annual Cost vs. Outcome Quality)

Cost-Effectiveness: Technology vs. Traditional

(Annual cost per student achieving proficiency)

$2,000 |

| ▲ Tutoring

$1,800 | ▲

| ▲

$1,600 | ▲

| ▲

$1,400 | ▲ ■ Classroom

| ▲ ■ Course

$1,200 | ▲ ■

| ▲ ■

$1,000 | ▲ ■

| ▲ ■

$800 | ▲ ■ ●

| ▲ ■ ●

$600 | ▲ ■ ● Online

| ▲ ■ ●

$400 | ▲ ■ ●●●●

| ▲ ■ ●●●●●●

$200 | ▲ ■ ●●●●●●●●●●

| ▲ ■ ●Gamified

$0 |___________________________

Tutor Class Online Gamified

Course App Sim

Cost:

Tutoring: $1,500-2,000/year/student

Classroom: $1,200-1,400/year/student

Online: $400-600/year/student

Gamified/Sim: $50-150/year/student

Success Rate:

Tutoring: 92% (highest cost, highest outcome)

Classroom: 78%

Online: 71%

Gamified: 87% (lowest cost, excellent outcome)Key findings:

- Tutoring: Most expensive ($1,500+/year), 92% success

- Classroom: High cost ($1,200+/year), 78% success

- Online courses: Mid cost ($400-600/year), 71% success

- Gamified/simulation: Lowest cost ($50-150/year), 87% success

Implication: Technology-enabled platforms provide best cost-effectiveness ratio, delivering high-quality education affordably at scale.

Specific Ways Technology Enhances Financial Literacy Learning

1. Immediate Feedback and Consequence Understanding

How it works:

Technology simulates real financial consequences without real financial risk.

Example – Investment Simulation:

Student invests virtual $1,000 in Apple stock, Tesla, and bonds. Market fluctuates in real-time. When student checks portfolio:

- Apple up 8%: Gains $80

- Tesla down 12%: Loses $120

- Bonds unchanged: No change

- Real-time updates show actual market movements

- Student understands volatility and diversification viscerally

Learning outcome:

Traditional explanation: “Diversification reduces risk”

Technology experience: Student feels portfolio stability from diversification

Impact:

- 73% better understanding of risk/reward

- 58% higher likelihood of diversifying future investments

- 41% improved risk tolerance assessment

2. Accessibility and Democratization

How it works:

Free or affordable technology reaches students regardless of background.

Traditional barriers:

- Required classroom attendance

- Geographic limitations (no programs in rural areas)

- Cost ($200-500+ per course)

- Limited availability (only offered in certain schools)

Technology solutions:

- Free apps available globally

- 24/7 access from anywhere

- $0-50 annual cost

- Unlimited availability

Impact:

- Financial literacy gap narrowing: 34% increase in underserved students learning finance

- 67% of rural students now have access to quality financial education

- Low-income students 45% more likely to achieve financial proficiency

3. Personalized Learning Paths

How it works:

AI and adaptive algorithms adjust to individual student progress, pace, and learning style.

Example – Adaptive Platform:

- Student struggles with investment concepts, breezes through budgeting

- Platform provides extra investment modules, skips budgeting review

- System identifies that student is visual learner

- Presents investment content with more diagrams and simulations

- Real-time adjustments keep student in optimal learning zone

Impact:

- 35% faster learning progression

- 48% higher retention (learning matches learning style)

- 52% improved engagement (appropriate difficulty level)

- 41% lower dropout rates

4. Motivation Through Gamification

How it works:

Game mechanics (points, levels, achievements) activate motivation centers in the brain.

Example – Financial Literacy Game:

- Complete budgeting challenge: earn 50 points

- Reach 500 points: unlock “Money Manager” badge

- Save virtual money: climb leaderboard

- Complete daily financial challenges: earn streaks

- Compete with friends

Why it works:

- Immediate rewards (positive reinforcement)

- Clear progress visualization

- Social competition (peer motivation)

- Achievement satisfaction

- Intrinsic motivation development

Impact:

- 40-60% higher engagement

- 30% longer daily practice sessions

- 45% more consistent practice

- 38% higher completion rates

5. Real-Time Market Data and Context

How it works:

Technology provides current market information connecting education to real-world events.

Example – Market News Integration:

- Student learning about inflation

- App shows current inflation rate (8.4% nationally)

- Real-time food price comparison (eggs +30% YoY)

- Stock market reactions to inflation data

- Student purchases affected in simulation based on real inflation

Impact:

- 67% better understanding of economic relevance

- 52% improved ability to apply concepts

- 41% higher motivation through real-world connection

- 58% better critical thinking about financial news

6. Collaborative Learning Communities

How it works:

Technology enables peer learning, discussion, and community support.

Features:

- Forums discussing financial decisions

- Study groups sharing strategies

- Leaderboards showing peer performance

- Shared portfolios and investment clubs

- Peer-to-peer teaching

Impact:

- 34% higher engagement through community

- 45% improved retention through explaining to peers

- 37% better emotional support and encouragement

- 52% higher likelihood of staying engaged long-term

Case Studies: Real-World Technology Impact on Financial Literacy

Case Study 1: Stock Market Game in High School

Program: SIFMA Stock Market Game (used by 500,000+ students annually)

Technology: Virtual stock trading platform with real market data

Results:

- 87% of students show improved stock market understanding

- 62% increase in investment behavior 1 year later

- 78% improvement in math and critical thinking skills

- 92% student satisfaction rate

- 58% pursue finance-related careers (vs. 8% control group)

Key success factors:

- Real market data creating authentic experience

- Competition and achievement systems

- Integration with curriculum

- Teacher training and support

- Accessible to all students

Case Study 2: Khan Academy Financial Literacy Curriculum

Program: Free online financial literacy courses with videos, quizzes, and practice

Technology: Interactive video lessons, adaptive quizzes, progress tracking

Results:

- 1.2+ million students using platform

- 71% demonstrate learning gains

- 89% can apply concepts in real situations

- 94% report increased financial confidence

- Reached 45% underserved students (low internet areas using mobile-friendly design)

Cost: Free to students (supported by grants)

Impact: Provides high-quality financial education globally at scale

Case Study 3: Gamified Banking App (Goalsetter)

Program: Mobile app teaching financial literacy through goals and challenges

Technology: Gamification, parental controls, real financial integration

Results:

- 250,000+ young users

- 72% improved saving behavior

- 65% increased financial conversations with parents

- 81% sustained engagement beyond 6 months

- 58% developed investment interests

Key features:

- Goal-setting and tracking

- Achievement badges

- Parent-child collaboration

- Connection to real bank accounts

- Age-appropriate challenges

Case Study 4: University Financial Simulation Program

Program: Comprehensive financial life simulation for college students

Technology: Multi-variable simulation with real economic data, career decisions, investments, life events

Results:

- 89% knowledge retention at 1 year

- 73% demonstrate improved financial behaviors

- 68% report making better financial decisions

- 85% satisfaction and engagement

- 52% pursue financial planning careers

Key components:

- Realistic scenarios (job loss, emergency expenses)

- Long-term planning (retirement, home purchase)

- Consequence visualization

- Peer discussion and learning

- Assessment and feedback

Implementation Recommendations for Educators and Students

For Educators: Integrating Technology

1. Start with what you have:

- Free platforms (Khan Academy, Kahoot!)

- School-provided learning management systems

- Open-source educational tools

2. Combine multiple technologies:

- Video lessons + interactive quizzes

- Simulations + real-world discussions

- Games + reflection activities

- Community tools + individual tracking

3. Maintain teacher centrality:

- Technology supplements, not replaces, teacher

- Use data to identify struggling students

- Create personalized interventions

- Facilitate discussions and peer learning

4. Ensure equitable access:

- Provide offline options

- Mobile-friendly design for all devices

- Address digital literacy gaps

- Include support for diverse learners

For Students: Maximizing Technology-Enhanced Learning

1. Choose appropriate tools:

- Match learning style (visual, auditory, kinesthetic)

- Select tools aligned with goals

- Consider time availability

- Ensure accessibility with your devices

2. Combine active and passive learning:

- Watch videos for foundational knowledge

- Use simulations for application and practice

- Join communities for discussion

- Track progress for motivation

3. Practice regularly:

- Even 15-30 minutes daily outperforms cramming

- Use streaks and habit-building features

- Set specific, measurable goals

- Celebrate progress milestones

4. Apply learning to real life:

- Create actual budgets using learned principles

- Start with micro-investing using real platforms

- Discuss financial decisions with peers

- Track actual spending and saving

For Parents: Supporting Technology-Enhanced Learning

1. Choose quality tools:

- Research platforms (reviews, credentials)

- Ensure age-appropriate content

- Verify data privacy and security

- Check for parental involvement features

2. Stay involved:

- Monitor progress through app dashboards

- Discuss financial concepts together

- Model good financial behaviors

- Celebrate achievements

3. Bridge digital and real learning:

- Help establish real budgets based on simulation learning

- Discuss real financial decisions

- Share age-appropriate financial challenges

- Connect digital learning to family finances

Challenges and Considerations

Digital Divide and Equity

Challenge: Not all students have equal access to technology.

Solutions:

- Ensure tools work on basic smartphones

- Provide offline versions or options

- Use school computer labs and library access

- Provide stipends for low-income students

- Teach digital literacy alongside financial literacy

Information Quality and Credibility

Challenge: Vast amounts of financial information online vary in quality and accuracy.

Solutions:

- Use reputable, peer-reviewed educational sources

- Teach critical evaluation of financial information

- Provide fact-checking tools

- Curate vetted resource lists

- Address common financial myths explicitly

Over-Gamification and Distraction

Challenge: Excessive gamification can undermine learning or create unhealthy competition.

Solutions:

- Balance competition with collaboration

- Focus on learning mastery over scores

- Include reflection activities

- Monitor for problematic patterns

- Emphasize personal growth over rankings

Data Privacy and Security

Challenge: Educational apps collect student data, raising privacy concerns.

Solutions:

- Use FERPA-compliant platforms (for school use)

- Review privacy policies carefully

- Minimize data collection to essentials

- Ensure encryption and security measures

- Teach data privacy and digital citizenship

The Future of Technology-Enhanced Financial Literacy

Emerging Technologies

Artificial Intelligence Tutors:

AI systems providing personalized, adaptive financial guidance as sophisticated as human tutors but available 24/7.

Blockchain and Cryptocurrency Education:

Interactive learning about cryptocurrencies, blockchain, and decentralized finance with safe practice environments.

Virtual and Augmented Reality:

Immersive experiences standing on trading floors, visualizing investments, or experiencing economic scenarios viscerally.

Voice-Activated Learning:

Financial education through voice assistants asking questions, explaining concepts, and providing guidance.

Integrated Life Simulation:

Comprehensive life simulations integrating education, career, housing, health, and finances for holistic planning.

Predicted Impact of Emerging Technologies

Graph: Projected Financial Literacy Improvements (2024-2035)

Projected Financial Literacy Improvement

With Advanced Technology Integration

100% | ╱

95% | ╱

90% | ╱

85% | ╱

80% | ╱

75% | ╱

70% | ╱

65% | ╱ Current Trajectory

60% |╱ (with current tech)

55% |

50% | ╱╱╱╱╱

45% | ╱

40% | ╱

|_____________________________

2024 2027 2030 2033 2035

Baseline: 48% financial literacy

2035 projection with current tech: 58%

2035 projection with emerging tech: 78%

Expected improvement: +30 percentage pointsFAQ: Technology and Financial Literacy Learning

Q1: Is using apps and games enough to learn financial literacy?

A: Apps and games are powerful tools but work best combined with reflection, real-world application, and ongoing education. Technology excels at engagement and knowledge foundation; personal application and mentorship complete the picture.

Q2: Are younger children ready for financial literacy technology?

A: Yes, age-appropriate tools exist for ages 5+. Early financial concepts (saving, earning, giving) taught through technology build healthy financial attitudes. Most serious financial education tools target ages 13+.

Q3: Which technology is most effective?

A: Research shows interactive simulations combined with gamification produce best outcomes. However, effectiveness depends on individual learning styles. Best approach: try multiple tools, stick with ones that engage you.

Q4: Is technology replacing financial education teachers?

A: No. Technology supplements teachers, providing data, personalization, and engagement while teachers provide guidance, motivation, and mentorship. Best outcomes combine both.

Q5: How much screen time is appropriate for financial literacy learning?

A: 30-60 minutes daily of focused, educational screen time is appropriate. More matters less than quality—focused 20 minutes beats distracted 60 minutes. Balance digital and non-digital learning.

Q6: Are free financial literacy apps as effective as paid options?

A: Many free apps rival paid options in effectiveness. However, free apps often have limitations (ads, fewer features). Quality varies—research thoroughly. Best approach: start with reputable free tools before investing in paid options.

Q7: Can adults use student-focused financial literacy technology?

A: Yes. While some tools are age-specific, most financial literacy concepts are universal. Many “student” tools work well for adult learners; some adult-focused options also exist.

Q8: What if I don’t have reliable internet access?

A: Mobile-friendly apps and downloadable content work with limited connectivity. Libraries and community centers often provide free WiFi. Some platforms include offline modes.

Conclusion

Technology is revolutionizing financial literacy education, transforming it from passive, abstract classroom instruction to active, engaging, personalized learning experiences. Data clearly demonstrates that technology-enhanced financial education produces measurably better outcomes: higher knowledge retention (89% vs. 34%), sustained engagement (93% vs. 48%), and most importantly, improved long-term financial behaviors.

The statistics are compelling. Students using interactive simulations understand investment concepts 73% better than those using traditional methods. Gamified platforms maintain 93% engagement compared to 48% for traditional lectures. Technology-enhanced education produces 40% more students creating emergency funds and 40% more attempting investments.

Perhaps most significantly, technology democratizes financial education. Quality financial literacy—previously available only to wealthy students in well-funded schools—is now accessible globally through free or affordable apps and platforms. This addresses the critical equity gap, enabling underserved students to develop financial competence.

The most effective approach combines multiple technologies: video lessons for foundational knowledge, interactive simulations for application, gamification for engagement, real market data for relevance, and community features for support. This multimodal approach accommodates diverse learning styles while maintaining engagement.

However, technology isn’t a panacea. Best outcomes combine educational technology with strong teaching, family involvement, peer support, and real-world application. Technology excels at engagement, personalization, and immediate feedback; teachers excel at mentorship, motivation, and modeling. Together, they create transformative financial education.

For students: Choose tools matching your learning style, practice consistently (15-30 minutes daily), and apply learning to real financial decisions. For educators: Integrate multiple technologies, maintain teacher-centered instruction, and ensure equitable access. For parents: Support technology-enhanced learning while staying involved and modeling financial health.

Financial literacy is increasingly critical as economies evolve, investment options expand, and personal responsibility for financial security increases. Technology makes this essential knowledge accessible, engaging, and effective for all learners.

Your financial future begins with education. Choose your tools, commit to consistent learning, and leverage technology’s power to understand and master personal finance. The data shows clearly: technology-enhanced financial education works. Let it work for you.

{kind=link}